In traditional finance, market liquidity is underpinned by the repo and securities lending markets. These infrastructures allow institutions to:

- Borrow cash against high-quality collateral (repo)

- Borrow securities to facilitate short selling, arbitrage, or market making (securities lending)

The system is vast, predominantly OTC, and accessible primarily to regulated institutions. Transactions rely on bilateral agreements, counterparty trust, and settlement cycles typically operating on T+1 or longer.

On-chain lending protocols represent a structurally similar mechanism, rebuilt as open financial infrastructure. They enable participants to:

- Supply digital assets and earn yield, economically comparable to securities lending or reverse repo activity

- Borrow assets against posted collateral in real time, similar to repo financing

The economic logic remains familiar: capital is made productive by temporarily transferring liquidity in exchange for compensation. What changes is the infrastructure.

Unlike the bilateral agreements that characterize traditional markets, on-chain lending venues are governed by deterministic smart contracts. The underlying economic principle remains familiar: overcollateralization. To borrow $100 worth of an asset, a participant must post collateral exceeding that amount. If the collateral value declines and breaches a predefined maintenance threshold, the position is automatically liquidated by the protocol.

System solvency is therefore maintained through transparent, rule-based collateral management rather than discretionary credit assessment or counterparty underwriting.

The lending protocol types

The on-chain collateralized credit ecosystem is broadly structured around two primary architectural models: monolithic and modular frameworks. The distinction between them lies primarily in how risk is pooled, isolated, and priced, as well as how liquidity is allocated across markets.

These structural choices materially impact:

- Capital efficiency

- Risk transmission across assets

- Governance complexity

- Suitability for institutional strategies

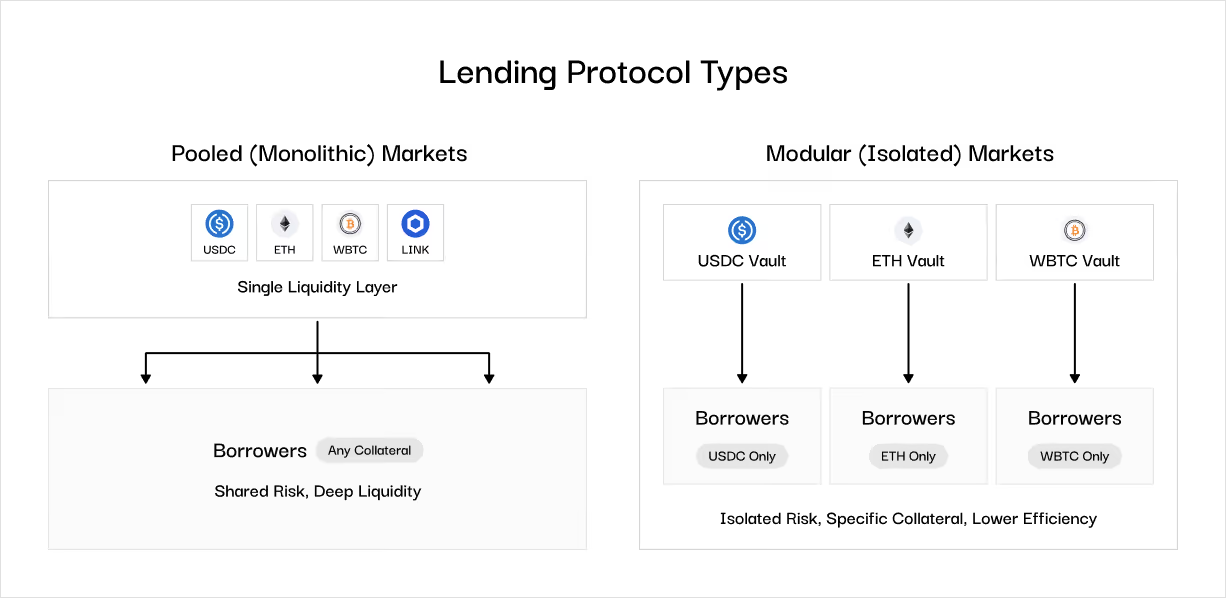

Pooled (Monolithic) Markets

Protocols such as Aave and Fluid operate under a pooled model. In this structure, all assets reside within a single liquidity layer. If you lend USDC, your capital is pooled with that of all other USDC lenders.

The advantage is deep, immediately accessible liquidity for borrowers across all accepted collateral types. The trade-off is that risk is shared: if a niche collateral asset within the pool fails, any resulting shortfall can, in theory, impact all USDC lenders.

Isolated & Modular Markets

The primary players in this category include Euler and Morpho. These protocols enable the isolation of individual markets, allowing lenders to exercise granular control over the specific collateral types to which they are exposed. For example, a lender may choose to supply capital exclusively against WBTC as collateral.

The trade-off is lower capital efficiency. If borrowing demand for that particular collateral is limited, the supplied capital may remain underutilized. By contrast, a pooled model enhances capital efficiency by aggregating borrowing demand across all accepted collateral types.

From discretionary to rule-based system

In traditional markets, counterparty risk is largely opaque. Market participants often do not know that a counterparty is insolvent until a default occurs, by which time the collateral available for liquidation may already have lost significant value. By contrast, on-chain lending protocols are transparent at all times and algorithmically liquidate collateral as soon as it breaches predefined risk thresholds.

Additionally, traditional markets are gated and typically settle on a T+1 or T+2 basis, whereas on-chain protocols settle atomically and operate on a permissionless basis.

This structural transparency materially alters the risk profile. Collateral ratios, utilization levels, and system-wide exposure are observable in real time, enabling continuous monitoring rather than periodic reporting. Margin calls are not negotiated — they are enforced automatically.

While this does not eliminate risk, it shifts the framework from discretionary and relationship-driven credit assessment to rule-based collateral management embedded directly into market infrastructure.

Digital lending in modern asset management

A Source of Yield

For asset managers, on-chain lending markets represent a programmable money market infrastructure. By supplying stablecoins or major digital assets into lending protocols, managers earn floating rates derived from borrower demand. These yields are market-driven, transparent, and continuously adjustable based on utilization. Unlike traditional cash management, where yield is often constrained by banking relationships and operational friction, on-chain lending enables immediate deployment of idle assets into collateralized credit markets, creating an efficient baseline return within a broader portfolio strategy.

Tactics

For asset managers, lending protocols are not only a source of yield but also a core tool for capital efficiency and portfolio construction. Beyond passive income generation, they enable more advanced positioning strategies:

Leverage

Lending markets provide the primary mechanism to source leverage on-chain without relying on derivatives. To construct bullish exposure to ETH, a manager can deposit ETH as collateral, borrow USDC, purchase additional ETH, and redeposit it. This “looping” process increases net exposure to ETH price movements. Some modern protocols, such as Fluid, allow this leverage to be executed as a single atomic transaction.

Shorting

By borrowing a specific asset such as ETH and selling it for stablecoins, a manager effectively establishes a short position. If the asset price declines, it can be repurchased at a lower price to repay the loan. The difference between the initial sale price and the repurchase price represents the profit.

Carry Trades

There is a broad range of yield-bearing assets available on-chain. For example, sUSDe represents a tokenized basis trade strategy. A manager may deposit sUSDe as collateral and borrow USDC against it. The spread between the yield earned on sUSDe and the borrowing cost of USDC constitutes the net carry. This position can also be looped to amplify exposure to the yield differential.

Minimizing Cash Drag

In traditional finance, idle cash often remains in custodian accounts earning minimal return. On-chain, idle stablecoins such as USDC or USDT can be deployed into lending markets immediately to generate yield until redeployed elsewhere, significantly reducing cash drag within the portfolio.

Understanding the risks

While lending protocols are foundational to on-chain finance and widely used across DeFi, they carry risks that require careful assessment.

- Liquidation Risk

If the value of posted collateral falls below the required maintenance threshold, the protocol automatically liquidates the position to repay the outstanding debt. Unlike a traditional margin call, where a broker may provide time to post additional collateral, on-chain liquidations are immediate and autonomous. They also involve a liquidation penalty, typically ranging from around 1% in more capital-efficient protocols such as Fluid to 5–10% in earlier-generation designs. - Smart Contract Risk

Lending protocols are software systems, and vulnerabilities in their logic or implementation can lead to unintended outcomes. That said, lending markets — alongside decentralized exchanges — are among the most battle-tested primitives in DeFi, securing billions of dollars in assets over multiple market cycles. - Utilization Risk

To maximize capital efficiency, most lending protocols deploy deposited assets to borrowers. If 100% of the liquidity in a pool is utilized, lenders may be temporarily unable to withdraw their deposits until borrowers repay or new liquidity enters the market. This should be distinguished from insolvency: it represents a liquidity constraint in which capital is temporarily locked, not impaired. - Solvency Risk

In extreme tail scenarios, collateral values may decline more rapidly than liquidations can be executed. If the outstanding debt exceeds the value recovered from collateral, the protocol may accumulate bad debt. In such cases, losses are often socialized across the pool, meaning lenders ultimately absorb the shortfall.

Leveraging Lending Markets with Enzyme Onyx

For managers targeting enhanced yield or specific risk exposures in emerging markets such as Morpho or Fluid, Enzyme Onyx provides the flexibility to integrate with any modern lending protocol within a tokenized fund structure.

This enables strategies to access early-stage opportunities across evolving on-chain credit primitives, without being constrained by a predefined or static integration framework.

Letsgetonchain is an independent DeFi researcher. With a background as a TradFi market maker, he transitioned to DeFi as a core contributor to a credit protocol. Today, he writes about DeFi’s market structures, mechanism design, and protocol economics.